1 The stock market has stumbled with the S&P 500 and Nasdaq declining year-to-date.

While tariffs have garnered the most attention, investors are also concerned about mixed economic signals including weak consumer confidence, hotter inflation, government worker layoffs, and more. Some are now wondering if there will be a recession, and President Trump did not rule out the possibility in recent interviews. How can investors maintain perspective in this challenging market and economic environment?

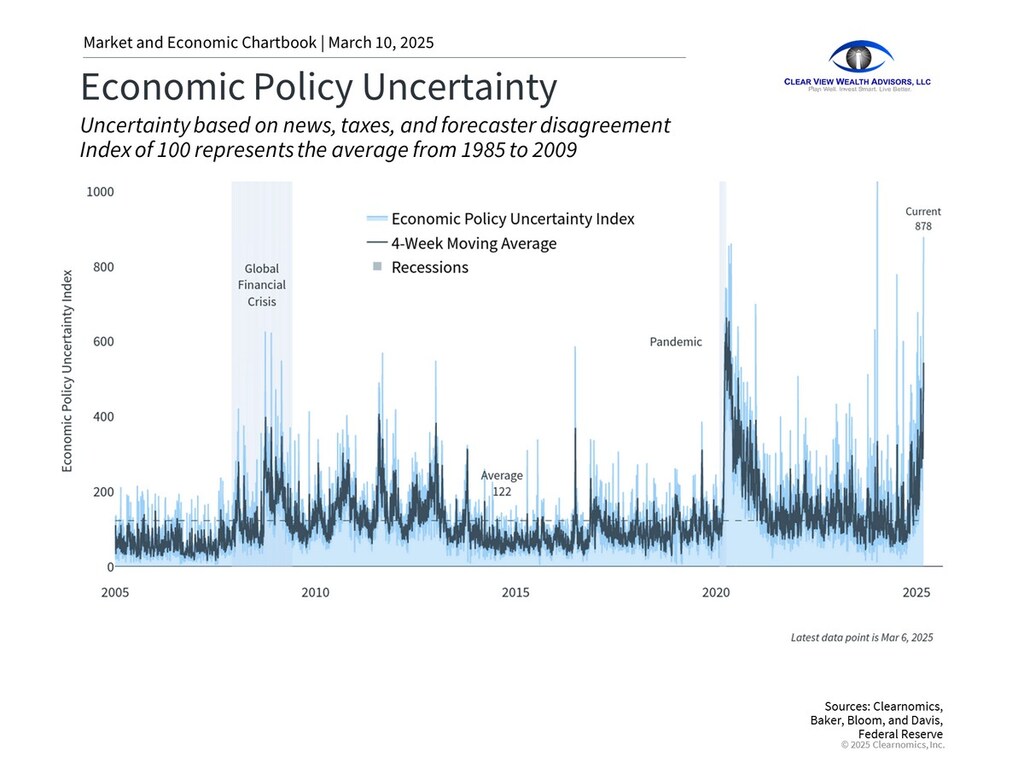

Chart: Uncertainty around economic policy has increased

To start, it is important to understand the difference between how individuals and households feel about the economy versus what drives financial markets. For example, when the prices of everyday goods and services increase, this can present challenges for our personal budgets. However, it may create potential opportunities in investments that can benefit from price increases. So, it's important as investors to remain objective and distinguish between our personal experiences with the economy and the factors that influence long-term investment returns.

While the economy and stock market are not the same thing, they influence one another in important ways. When economic growth is strong, corporate earnings tend to grow which can boost share prices, and vice versa. Similarly, stock and bond markets can sometimes serve as a leading indicator for the broader economy since they reflect the forecasts of millions of investors.

This does not mean that the market is always correct. It’s important to remember that some investors and economists have been predicting a recession for nearly three years. Just a year ago, many believed a recession would be imminent due to inflation. Even academic indicators of recession, such as the “inverted yield curve” or the “Sahm Rule,” have not proven to be reliable this time around.

Instead, not only has the economy grown steadily in the past few years, markets have also performed well. Despite the current pullback, the S&P 500 has gained over 60% since the market bottom in late 2022,

while the Nasdaq has risen 78%.

Of course, like a stopped clock that happens to be right twice a day, there will eventually be a recession. However, these examples show that predicting the timing of economic downturns is difficult. Investing based on the assumption of an economic downturn can lead to sub-optimal financial decisions, which is why it’s important to build portfolios that focus on long-term goals rather than near-term uncertainties.

2 Why have recession concerns risen?

Historically, recessions occur when the business cycle enters its later stages, or an external shock takes place, such as a pandemic or financial crisis. The current business cycle has shown signs of slowing, but has not contracted just yet. Instead, a possible trade war represents an outside shock to consumers, businesses, and global supply chains. Additionally, slower growth - or even two consecutive quarters of negative growth - are quite different from situations like the 2008 global financial crisis or 2020 pandemic shutdown.

The administration has said there may be a period of short-term "turbulence" in the economy. Even if tariffs do not directly harm growth, they have created an environment of uncertainty, as shown in the chart above. And market investors and businesses hate uncertainty. The administration has acted more swiftly with broad tariffs compared to President Trump’s first term, making the outcome harder to predict. Only time will tell if tariffs reach rates not seen since the 1930s, or if agreements with major trading partners will be reached.

It’s important to remember that tariffs come in different "flavors." Some are "retaliatory" against what may be considered unfair practices by a trade partner. Others may be implemented to protect a domestic industry. Tariffs are often used as a negotiating tactic for broader policy objectives. In the past, market reactions to tariff announcements were more dramatic than their actual economic impact. In 2018, the market fell as tariffs were implemented, but earnings growth was still strong and GDP was almost 3% that year.

While this uncertainty may be uncomfortable and has led to market swings, it’s in periods of economic strength that policy shifts can be most easily absorbed.

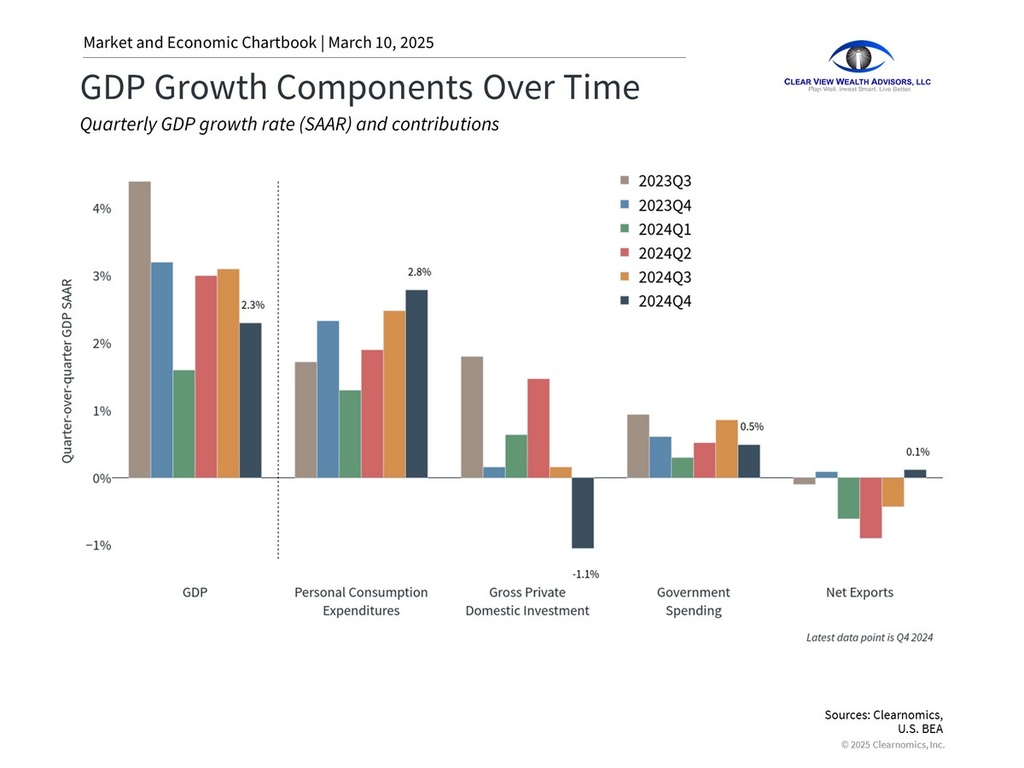

3 Chart: The economy has grown steadily despite investor fears

Beyond tariffs, the economic data is causing concern, including hotter-than-expected inflation and mixed jobs numbers. For example, the Consumer Price Index reversed course recently and rose above 3.0% for the first time since last summer.

Adding to this uncertainty, federal government jobs fell by 10,000 in February according to the Bureau of Labor Statistics, and more are expected. While federal workers account for less than 2% of the workforce, there is concern of ripple effects on the private sector and job growth overall. Despite this, the economy still added a healthy number of jobs in the latest report. While the markets have reflected the headlines of government layoffs, it'll take a while before they are actually reflected in data.

The price sensitivity of the consumer and their outlook on the job market have also worsened. Consumers now expect inflation of 3.5% over the next five years, the highest level since 1995, according to a University of Michigan survey. This has translated into feelings of deep pessimism about their financial situation in the next 5 years. And inflation expectations, if they take hold, will have an impact on consumer prices, interest rates, and wage pressure.

The irony is that markets have forgotten about the reasons for their post-election optimism: the possibility of pro-growth policies around manufacturing, energy, taxes, and regulation. As the chart above shows, consumer spending has driven the economy in recent years. Some economists hope that policy changes could boost business spending as well. An extension of the Tax Cuts and Jobs Act (TCJA) is currently being considered by Congress, and regulatory changes are in progress as well. Markets tend to ignore the long-term effects of tax and fiscal policies and focus on the nearer-term impact on profits, earnings, and stock prices

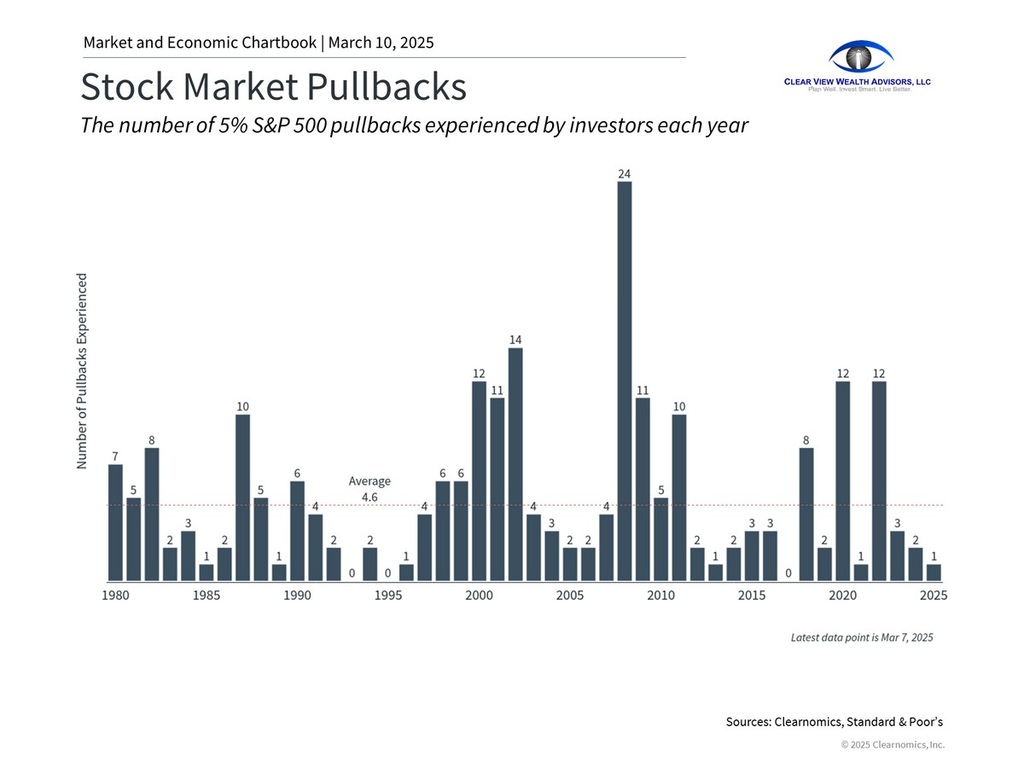

Chart: The S&P 500 experiences pullbacks on a regular basis

While the thought of a recession can be unpleasant, it’s important to remember that periods of slower economic growth are a natural part of the business cycle. Forecasts are not always correct, and even when they are, markets do not always behave in expected ways. While the past is no guarantee of the future, the market declines and subsequent sharp recoveries in 2020 and 2022 are recent examples of situations where markets can quickly change their tune.

Similarly, short-term market pullbacks are a natural part of investing. As the accompanying chart shows, the S&P 500 experiences pullbacks on a regular basis, even as it has risen in the long run. It’s important to maintain a broader perspective amid heightened economic concerns.

The bottom line? The possibility of a recession is back on investors’ minds but long-term investors should maintain a broader perspective. While tariffs have increased uncertainty and some economic data has been mixed, history shows that staying invested through challenging periods is the best way to achieve financial goals.

1 Standard & Poor’s and Nasdaq have declined 1.9% and 5.8%, respectively, as of March 7, 2025

2 S&P 500 price return from September 20, 2022 to March 7, 2025

3 Nasdaq Composite price return from December 22, 2022 to March 7, 2025

Steve's View ...

As unsettling as it is to see repeated headlines of market drops, it isn't unusual. In fact the average year sees the stock market drop -13.5%. But in most years, the market indices still end up in positive territory, averaging 9% gains.

Admittedly, the S&P 500 companies collectively have a forward price-earnings (P/E) ratio of about 22.4, which is above the historical average of about 16 and slightly below the 24.5 reached at the height before the Tech Bubble peaked in 2000. While these valuations are not outside the range, they are indicating that the market is less attractive. Using backward-looking data like the Shiller PE, a measure based on inflation-adjusted earnings, the market seems to not necessarily be in bubble territory. This is why investors need to maintain diversification across asset classes and markets, domestically and globally.

And despite the recent pain, these corrections in US stock markets will create opportunities for investors who have cash and are able to take advantage of these price changes.

Risks of Recession, Inflation, or Both?

Despite the recent headlines, increasing government unemployment hasn't yet filtered through to the data. While there has been an increasing number of layoffs in hi-tech over the past year or so, the overall unemployment rate (4.0%) is still near the lowest point in over 50 years.

The Sahm Rule noted above is a recession indicator based on a sudden increase in the three-month moving average for unemployment. While not perfect, it has indicated a recession when triggered in June 2001, February 2008, and April 2022. In 2021/2022, the indicator peaked but no recession followed. While the indicator triggered again in July 2024, there has not been evidence of a recession yet. In fact, the indicator has dropped though that may change if recent government layoffs are compounded by increased unemployment in the private sector. At this time though, that doesn't appear to be the case.

Yield curves, the difference between the 2-year and 10-year US Treasury rates, are another recession indicator. When the rate for the 2-year is above the 10-year, it's usually a sign of an imbalance in the market and a likely recession. Since last quarter, this yield curve has improved as shorter-term rates have dropped below longer-term rates. This would normally be considered a good sign that a recession is not on the horizon. But the path of interest rates will depend on policy uncertainty and economic growth.

Leading Economic Indicators (LEI) are another tool to read the tea leaves. Usually, when these indicators drop or turn negative, the slowdown in future economic growth usually means a recession follows. While this has traditionally been the case, a drop in the LEI in 2020 didn't lead to a recession. Right now, the current LEI is -2.6% which would indicate the higher potential for recession.

The mixed signals from the Sahm Rule, yield curve, and LEI index can lead to different conclusions. I believe that there are still a number of positives for continued though slow economic growth through 2025 including positive corporate earnings and continuing consumer demand. That said, continued policy uncertainty will very likely lead to a recession at some point after Q1 in 2026. In the nearer term, the Fed will likely hold off on changing its interest rate stance until after getting a couple of quarter's of data. At that point, the impact of immigration and trade policy changes will be better known. I think that they'll be more inflationary than expected and the Fed will begin to increase rates in the last quarter of 2025.

Portfolio Moves

Despite the recent unsettling moves, investors need to keep perspective. As long as you have a globally diversified portfolio, you'll likely weather the short- and long-term changes in the markets. Clearly, market volatility has increased under this Administration. That isn't going to change or settle down any time soon.

To meet the challenges of this period, the MarketFlex portfolio models have increased cash levels above the 1%-3% typical range. Depending on investor risk profile, this has increased to 5% to 10% or more for certain investors in retirement. There are a number of high-yield money market funds to use to park funds here. For those who want downside protection while still participating on any possible upside and are not in need of income from these parked funds, I've moved funds into "100% buffer" ETFs from Innovator ETFs as a cash alternative.

Alternatives will continue to play a strong role in all models. These include commodities for inflation protection (through COM and GLD ETFs). Defined-outcome or "buffer" ETFs and a broad-based managed futures ETF (RSST) will continue to be used to hedge market volatility. Private and alternative credit continue to do better than broad bond index funds. Real estate funds focused on housing and storage as well as infrastructure offer bright spots in this space as well.

I'll note that the income focus of the MarketFlex portfolio which uses high-yielding closed-end funds (CEFs) like USA and JEPI has stood up well during the recent market turbulence. While share prices have dropped along with the underlying stocks held in these and other low-cost index funds, the higher yields earned have helped to prop up and lessen the impact of recent market volatility.

Bottom Line: Stay diversified. Consider alternative income. Don't throw everything into cash.

Information provided in these materials has been drawn from resources deemed reliable. Clear View Wealth Advisors, LLC ("RIA firm") and Steve Stanganelli, CFP(r) ("Advisor") may provide additional commentary accompanying the materials. Any commentary by the source materials may differ from opinions expressed by the Advisor or RIA firm. Commentary and opinions of the Advisor and RIA firm are provided in good faith.

Chart books, newsletters, and related materials are distributed for general informational and educational purposes only and are not intended to constitute legal, tax, accounting or investment advice. All investments involve risk, including loss of principal, and past performance of a security, cryptocurrency, financial product, or strategy does not guarantee future results. Neither the RIA Firm nor the Advisor represent that the securities, cryptocurrencies, products, or services discussed in any of these materials or related websites are suitable for any particular investor. You are solely responsible for determining whether any investment, investment strategy, security, cryptocurrency, or related transaction is appropriate for you based on your personal investment objectives, financial circumstances and risk tolerance. You should consult your business advisor, attorney, or tax and accounting advisor regarding your specific business, legal or tax situation.

Any investments or strategies mentioned may not be suitable for all investors. Investors should consider the investment objectives, risks, and charges and expenses of any investment before investing. Investors are advised to consult with their financial and/or tax advisors and refer to any prospectus for any investment.

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.