For many Americans, the status of the U.S. dollar reflects the country’s position in the world. However, the dollar has weakened in recent months amid trade and economic uncertainty, declining against a basket of major currencies to its lowest level in three years. This has renewed concerns that the dollar could lose its place in the global financial system.

For investors, understanding the dollar's role in global markets and the forces that influence it remains important for portfolio positioning. What factors are driving these recent currency moves, and how might they affect the dollar's long-term prospects?

Historical perspective on the dollar

The U.S. dollar has served as the world's primary reserve currency for the past century, since it overtook the British pound after World War I. Some investors worry that geopolitics, fiscal challenges such as the national debt, trade policies, or emerging alternatives such as the renminbi or cryptocurrencies could threaten this status.

While these are real concerns, it’s important to understand that these worries are not new and tend to resurface during periods of economic uncertainty. In the 1980s, Japan's economic boom led to speculation that the yen might challenge the dollar. The introduction of the euro in the 2000s, along with China's economic rise, sparked similar predictions. More recently, the emergence of cryptocurrencies has prompted questions about the future of traditional currencies like the dollar.

Despite these fears, the dollar has maintained its central role in global finance through many economic cycles. This resilience reflects the depth and liquidity of U.S. financial markets, the relative stability of American institutions, and the dollar's continued use in international trade and investment. In general, the dollar continues to be viewed as a safe-haven asset during times of global economic crisis.

When it comes to our daily lives, it’s natural to view a strong dollar as always being positive. For consumers, a strong dollar makes traveling abroad more affordable and lowers the cost of imported goods, potentially reducing consumer inflation. So, when it comes to buying foreign goods and services, having a strong currency helps.

However, there are negatives to a strong dollar as well, especially when it comes to selling our goods and services. A strong dollar can make U.S. businesses less competitive since their products become more expensive for overseas buyers, potentially hurting American manufacturers and farmers. This is why many countries are often accused of keeping their currencies artificially low in order to boost their exports.

It’s easy to see that the ideal currency level depends on a balance of factors and isn’t just about strength or weakness.

Many factors drive the value of the dollar

There are many ways countries can manage their currencies. Some, like the United States and the United Kingdom, allow their currencies to float freely, with exchange rates determined primarily by market forces. Others maintain fixed exchange rates by pegging their currency to another major currency, such as the U.S. dollar or euro, or keep the value within a range. This requires central bank intervention and is not always easy to maintain.

An important driver of currency values is international trade. When foreign investors purchase U.S. goods and services, they must first exchange their currency for dollars. All things being equal, this demand for a currency creates upward pressure on the currency, raising its value relative to other currencies. The opposite is true when Americans import more than we export: the dollar is sold for foreign currencies.

In a perfect world, trade between nations would balance.Oftentimes, one nation imports more from others resulting in a "trade imbalance" leading to a "trade deficit" by the importing nation and vice versa. But we don't live in a perfect world.

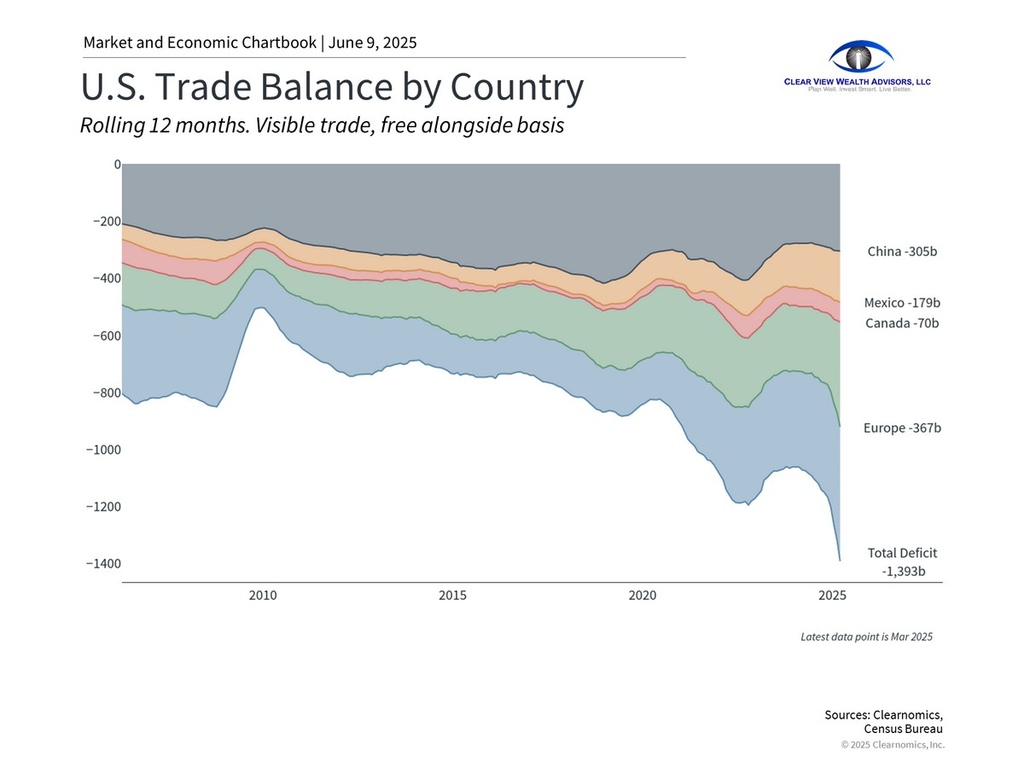

This is why a persistent trade deficit would normally lead to a weaker currency. As US consumers have imported more from overseas sources, we have had to trade in our dollars to purchase other currencies resulting in a higher supply of US dollars on the market. Following the laws of supply and demand, the price (value) of dollars has fallen (or depreciated). Over the past twelve months, the U.S. imported $1 trillion more than it exported, as seen in the accompanying chart. This trade imbalance has persisted for many years, partly because there is significant demand for dollars by central banks and foreign businesses.

Interestingly, recent tariffs have not resulted in a stronger dollar. Economic theory would normally suggest that U.S. tariffs on foreign goods would reduce imports, thus putting upward pressure on the dollar. However, not only did many companies stockpile foreign goods ahead of these tariffs, but other factors such as capital flows and political uncertainty impact the currency as well.

Trade represents only one component of the broader currency equation. Capital flows, interest rates, central bank policies, and international lending all contribute to global dollar demand. The complexity of these interactions explains why currency movements often seem disconnected from simple economic indicators.

For example, differences in interest rates are among the most important factors that influence currency values. When the Federal Reserve sets rates higher than other major central banks, it typically creates demand for dollars, since investors could shift their assets to higher-yielding Treasuries.In financial markets, this is known as a “carry trade.” This demand, in turn, will lead to an appreciation of the dollar compared to other currencies resulting in the ability to buy more imported goods and services which will contribute to the trade deficit.

Additionally, concerns about fiscal policy may also be weighing on the dollar. With the national debt approaching 120% of GDP and persistent budget deficits, some investors worry about the long-term sustainability of U.S. fiscal policy. Investors are concerned that such persistent deficits will require more bond issuance. To counter the increased supply of US Treasuries that would be issued, expectations are that investors will demand higher interest rates to compensate for the risk. While these concerns have not reached crisis levels per se, they add another layer of complexity when valuing the U.S. dollar.

The dollar has maintained its global role

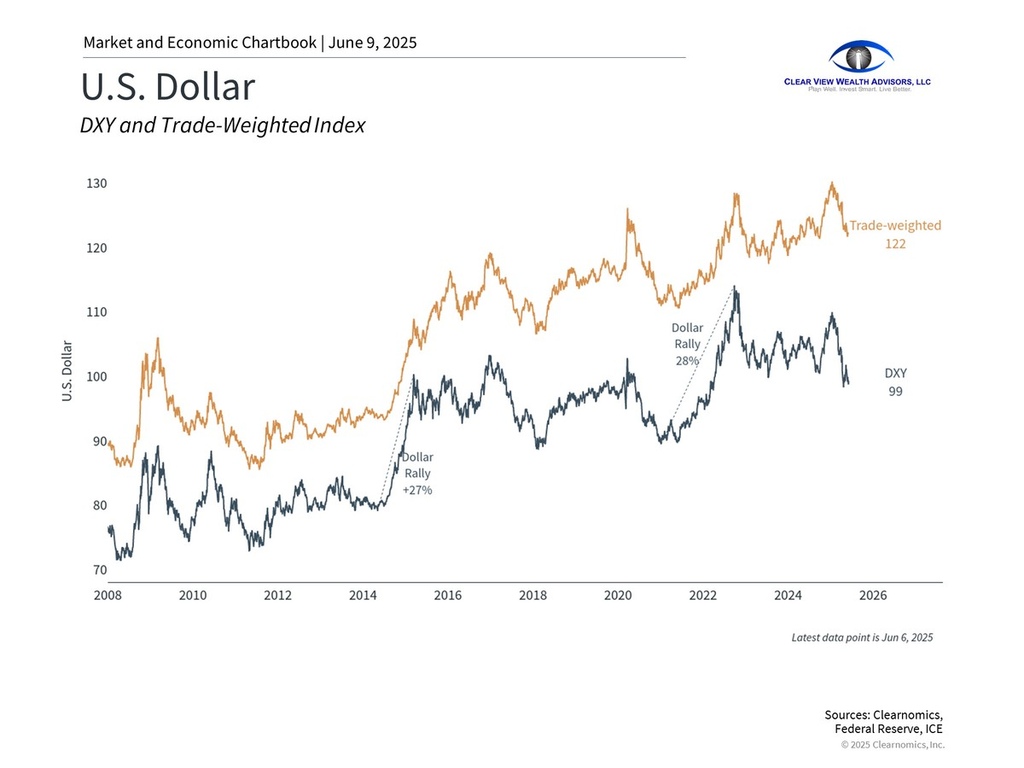

Given the many factors that influence its value, some perspective is needed when judging the current level of the dollar. While the dollar has declined to its lowest level in three years, zooming out shows that these levels are still near their strongest over the past twenty years. As always, it’s important to maintain a broader perspective and not overreact to recent moves.

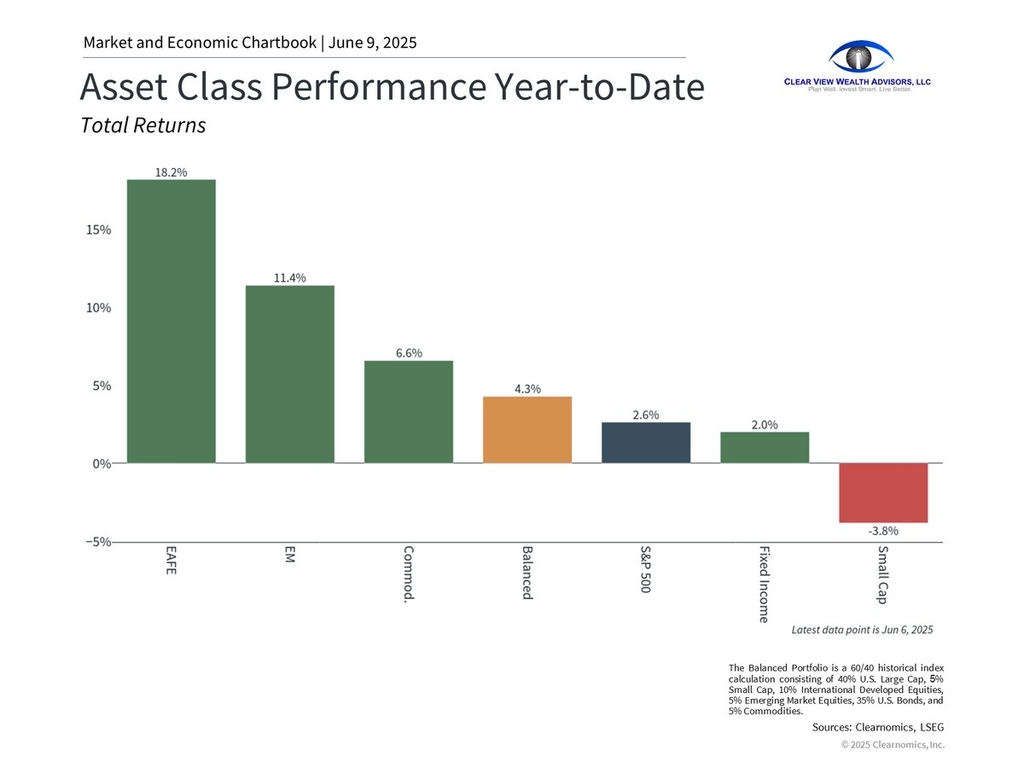

For investors, a somewhat weaker dollar has been positive this year for diversified portfolios. A falling dollar means that international investments are worth even more when converted back from their local currencies, boosting returns. The accompanying chart shows that the MSCI EAFE index of developed market stocks and the MSCI EM index of emerging market stocks have outperformed the S&P 500 this year.

The bottom line? Despite many legitimate concerns, the dollar continues to serve as the world’s reserve currency. Perhaps more importantly, it has helped to boost diversified portfolios this year. Investors should continue to maintain a long-term perspective on the dollar.

Steve's Portfolio View ...

With ongoing uncertainty regarding tariff, tax, and budget policy, the general outlook remains cloudy over the near term (three- to 6 months). While the consensus among many investment analysts is for two Fed cuts in the second half of 2025, much will depend on actual data from the impact of tariffs along with the impact of reductions in government spending in certain areas and federal employment.

Labor markets remain resilient though growth has been limited to a small slice of the market (hospitality and services mainly). Inflation expectations seem to have eased though actual inflation is still running hotter than the Fed's target. Recent forecasts by the Atlanta Federal Reserve indicate a 3.8% expansion in GDP for the second half of 2025. Clearly, this forecast coupled with fairly stable employment readings is not one of imminent recession. Cutting rates now would seem to be adding fuel to the fire and lead to accelerating inflation. In turn, this would not bode well for longer-duration bonds over time though it might help with lowering the trade deficit as imports become more expensive with an eventual rise in interest rates.

Current Market Themes

In this environment, it's likely best to overweight large-cap US growth stocks and underweight value stocks relative to the allocation appropriate for an individual investor's risk profile. Tactically, investor allocations should emphasize the "dividend" and "quality" factors.

Likewise, investors are advised to overweight investment grade bonds mainly through US Treasuries and underweight high yield bonds. For more detail, refer to the Market Desk Investment Analysis section of the Smart Money Insights & Blog of the CVWA LLC website.

For "Global Core" investors, the following are recommended general ranges of allocations:

- Moderately Conservative: 18% - 25% US Stock / 10% - 15% International Stock / 65% - 75% Bonds / Cash 0% - 10%

- Moderate/Balanced: 32% - 45% US Stock / 15% - 30% International Stock / 30% - 45% Bonds / Cash 0% - 10%

- Moderate Growth: 35% - 50% US Stock / 22% - 35% International Stock / 25% - 35% Bonds / Cash 0% -10%

Core investments can include:

- Vanguard Total Bond Market mutual fund (VBTLX) or Vanguard Total Bond Market ETF (BND) which may be combined with Vanguard Intermediate Term Corporate Bond ETF (VCIT)

- Vanguard European Stock Admiral shares mutual fund (VEUSX) or Vanguard FTSE Developed Markets ETF (VEA) or Vanguard Total International Stock Index with emerging market exposure (VTIAX)

- Vanguard Total Stock Market Index Admiral shares mutual fund (VTSAX) or Vanguard Total Stock Market ETF (VTI)

- Vanguard Dividend Appreciation Index Admiral shares mutual fund (VDADX) or Vanguard Dividend Appreciation ETF (VIG)

These allocations apply to the core holdings. Investors may want to keep cash set aside for future investing as "dry powder." Additional cash reserves needed for living expenses or as an emergency reserve are not part of these model allocations. A reasonably good option for cash is the Vanguard Cash Reserve Federal Money Market (VMRXX) with an approximate yield of 4.7% (as of 6/06/2025).

Information provided in these materials has been drawn from resources deemed reliable. Clear View Wealth Advisors, LLC ("RIA firm") and Steve Stanganelli, CFP(r) ("Advisor") may provide additional commentary accompanying the materials. Any commentary by the source materials may differ from opinions expressed by the Advisor or RIA firm. Commentary and opinions of the Advisor and RIA firm are provided in good faith.

Chart books, newsletters, and related materials are distributed for general informational and educational purposes only and are not intended to constitute legal, tax, accounting or investment advice. All investments involve risk, including loss of principal, and past performance of a security, cryptocurrency, financial product, or strategy does not guarantee future results. Neither the RIA Firm nor the Advisor represent that the securities, cryptocurrencies, products, or services discussed in any of these materials or related websites are suitable for any particular investor. You are solely responsible for determining whether any investment, investment strategy, security, cryptocurrency, or related transaction is appropriate for you based on your personal investment objectives, financial circumstances and risk tolerance. You should consult your business advisor, attorney, or tax and accounting advisor regarding your specific business, legal or tax situation.

Any investments or strategies mentioned may not be suitable for all investors. Investors should consider the investment objectives, risks, and charges and expenses of any investment before investing. Investors are advised to consult with their financial and/or tax advisors and refer to any prospectus for any investment.

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.